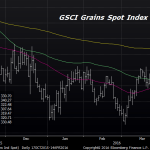

Seeing silver, sugar and soybeans forge strong price gains has historically hinted at inflation, but that type of forecast seems foolhardy in the current environment.

Trade Futures, Spreads and Options with Confidence.

Seeing silver, sugar and soybeans forge strong price gains has historically hinted at inflation, but that type of forecast seems foolhardy in the current environment.

The “talking heads” and “talking fund managers” are suggesting that the rally in commodities is done, unjustified and poised to be reversed.

Just when it appeared that the commodity markets were overbought and poised to correct, the US Fed was found to be on-hold “to at least June.”

We think that commodity markets were short-term and perhaps even intermediately overbought going into their recent highs.

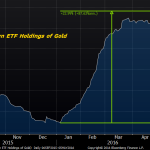

Just when it appeared that commodities were settling back on a deflationary track, leadership surfaced in fresh buying interest in gold, silver, platinum, soybeans, corn and crude oil.

The recent retrenchment in bean oil, crude oil, sugar, corn, equities, cattle, gold, platinum, palladium and copper as well as significant rallies in Treasuries and the Japanese yen mostly started around March 14th, and some have labeled the period since mid-March as a “crisis.”

An improvement in US and European manufacturing activity as well as news that the “official” Chinese PMI number climbed back into expansion territory for the first time in 8 months bodes well for a more sustainable global recovery effort.

Several weeks ago we spoke of a brightening of economic skies, but in this publication, we have to note some short-term vulnerability potential in markets that are overbought and/or markets that might be overly sensitive to a shift by the Fed back toward a more hawkish stance at upcoming FOMC meetings.

After a slight brightening of the skies, the US Fed has stepped in and stoked recovery efforts further with a reduction in the number of anticipated 2016 rate hikes and a nod to the importance of international headwinds in their future policy decisions.

The brightening of the economic skies continues, but the pace of improvement remains difficult to detect.