Play Turner’s Take Ag Marketing Podcast Episode 276

Podcast: Play in new window | Download

Subscribe: RSS | Subscribe to Turner's Take Podcast

If you are having trouble listening to the podcast, please click here for Turner’s Take Podcast episodes!

New Podcast

In this week’s podcast we go over the latest news in the grain and oilseed markets. We also take a look at the May WASDE from last week to get an idea of possible price ranges for old and new crop going forward. Make sure you take a list to Turner’s Take Podcast!

If you are not a subscriber to Turner’s Take Newsletter then text the message TURNER to number 33-777 to try it out for free! You may also click here to register for Turner’s Take.

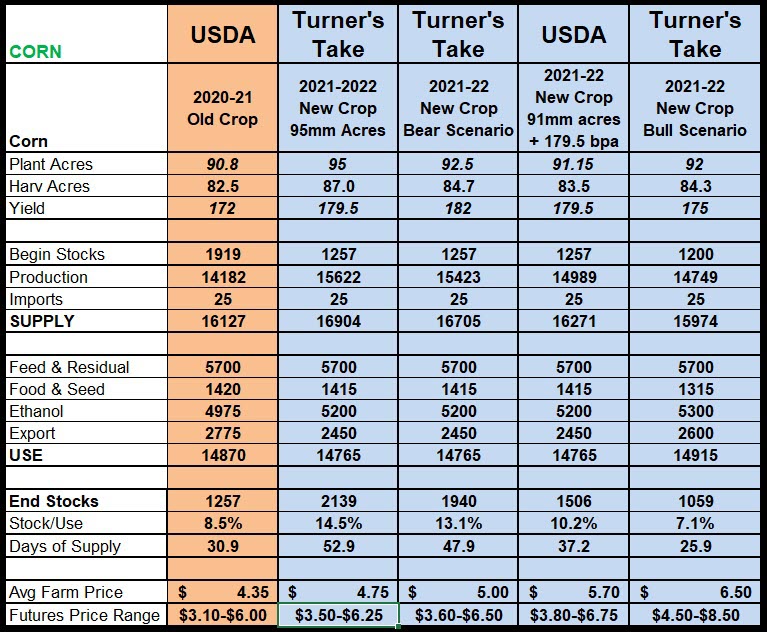

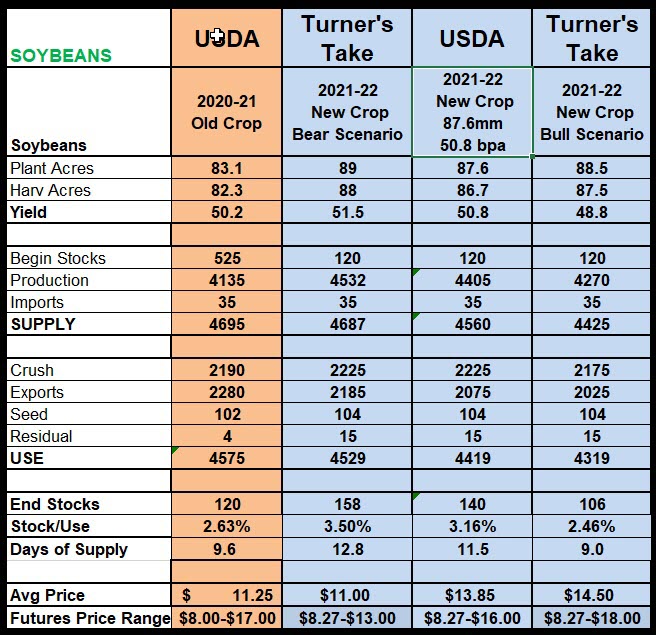

May WASDE

The May WASDE showed tight stocks for old crop and new crop soybeans. Even with additional acres or a better than trend line yield, soybeans will most likely be under 200mm bushel ending stocks for new crop. This keeps soybean prices elevated until the next South American harvest in 2022.

Corn is a different story. Adding a few million acres of corn could push new crop ending stocks to a 2.0 billion and prices into the $4s. A loss of 5 bpa this summer off the national yield could send new crop over $6 and maybe even $7. When corn is projected to have a 1.5 billion ending stock that means we are at 10% stock to usage. That is right on the line of adequate and tight stocks. A loss of 500mm bushels (6 bpa) or a gain of 500mm bushels (3mm acres) can have a huge impact on prices. It is the difference between burdensome stocks (over 2 billion) and very tight stocks (just over 1 billion).

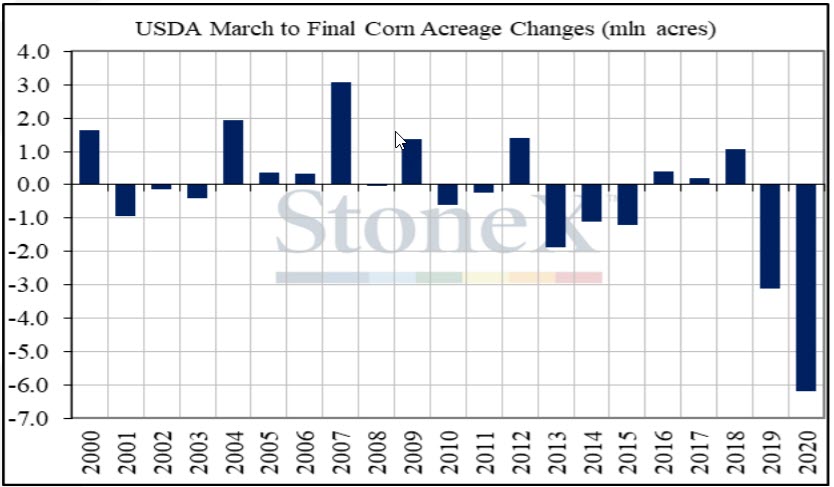

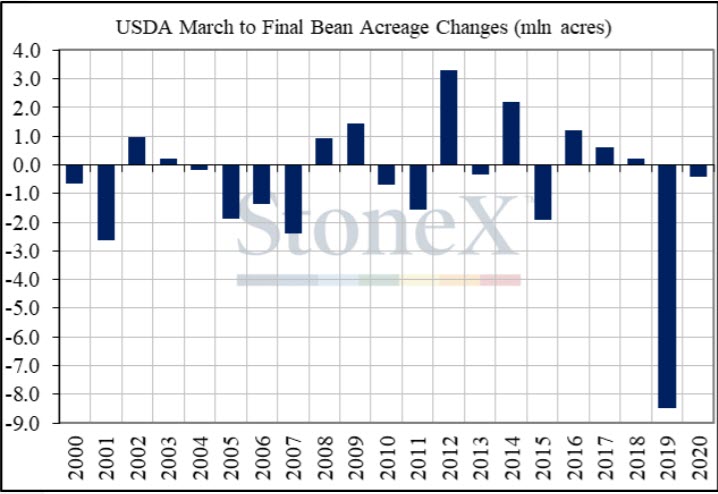

The charts on the bottom of this email show the net change of corn and soybean acres from the March to June report for the past 20 years. Only in 2007 was corn up 3mm acres (soybeans down 2mm) and in 2012 soybeans were up 3mm acres (corn up 1mm).

We haven’t even started to talk about new crop Chinese demand, the shortage of old crop corn in Europe, and the dry conditions in much of China’s top corn producing regions. We do think more wheat will be used for feed instead of corn but that can’t solve all the balance sheet issues. Good growing weather and more than a couple million acres could send new crop corn into the $4s. A serious weather threat and yield loss cold send the market much higher.

Interested in working with Craig Turner for hedging and marketing? If so then click here to open an account. If you are a speculative or online trader then please click here.

Corn Supply & Demand Scenarios

Soybean Supply & Demand Scenarios

Interested in working with Craig Turner for hedging and marketing? If so then click here to open an account. If you are a speculative or online trader then please click here.

About Turner’s Take Podcast and Newsletter

If you are having trouble listening to the podcast, please click here for Turner’s Take Podcast episodes! Craig Turner – Commodity Futures Broker 312-706-7610 cturner@danielstrading.com Turner’s Take Ag Marketing: https://www.turnerstakeag.com Turner’s Take Spec: https://www.turnerstake.com Twitter: @Turners_Take Contact Craig Turner

Risk Disclosure

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI does business as Daniels Trading/Top Third/Futures Online. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2023 StoneX Group Inc. All Rights Reserved

You must be logged in to post a comment.